Developing a business case (referred to interchangeably in this article as “BC” and “business analysis”) can be compared to a court trial. The participants select arguments, use or reject evidence, all in an effort to convince the judge and the jury of the validity of their case.

A lawyer’s argument can be structured in many ways and be more or less effective — likewise, there is no single, definitive formula for BC, but there are guidelines worth considering.

Tough Questions

In general terms, a business case is a proposal for a business change, presented in the form of a report and described in terms of costs and benefits. The development of a business case precedes large-scale implementation projects (e.g., an ERP system or one of its components) and aims to convince management to invest by presenting rational arguments (primarily financial ones).

A business analysis is not just a financial document. It is a structured set of answers to the following questions, among others:

- Why is this project necessary?

- What are the expected benefits of implementation?

- What are the available options, and what are the reasons for choosing or rejecting each one?

- What costs (financial resources, personnel, time) must the organization incur to ensure the project’s success?

- What are the risks?

- What impact will the decision not to launch the project (“do-nothing scenario”) have on the business?

When will the new solution be ready for operational use?

Business Case Checklist

- Have the business requirements been clearly defined?

- Have all the benefits been identified?

- Has the final outcome of the project been clearly defined?

- Does BC recommend a specific solution?

- Was the recommendation clearly justified?

- Have the cost and source of funding been determined?

- Have the risks to the project been identified?

- Have methods for reducing risks to an acceptable minimum been identified?

A business case for the shelf?

Business Case (BC) does not end once the project is launched; it requires ongoing review throughout the project. In particular, it is important to ask whether the business need that served as the basis for the BC still exists and whether the project is on track to achieve the results specified in the analysis.

This gives us the opportunity to change the scope of the project or even terminate it if warranted. BC is therefore also a tool for monitoring the project from a business perspective.

The reasons for preparing business analyses can vary. In the area of implementing and developing IT systems that support management, these are most often:

- BC for the implementation of an IT system (without assuming that it will be SAP),

- BC for the implementation of an integrated SAP system (or one of its components).

- BC for migration to a new technology (e.g., SAP applications from the ITS platform to WAS).

The goal of business case analysis is most often to answer a fundamental question: What will be the financial (costs and benefits) and business implications of deciding to implement the system?

The analysis is also intended to help plan the project, set priorities, and determine how to implement it.

How to Prepare the Business Continuity Plan for the Implementation of the SAP System?

A prerequisite for preparing a business case is assembling a team that includes representatives from both the business and IT departments. This team may be supported by external consultants who serve as moderators and, at the same time, as subject matter experts for the SAP system.

Let’s imagine that a company is faced with the decision to implement the mySAP HCM integrated system (this is the scenario where the choice of solution has already been made, and the Business Consultant focuses primarily on answering the question of whether the implementation is justified—“do or do nothing”).

Justifying the need to implement a human capital management system is no trivial task, especially since identifying the financial benefits requires combining knowledge of business processes with expert knowledge of the system and its configuration options.

The proposed content of such a BC is presented below:

- the project’s strategic objectives (including its contribution to the company’s strategy),

- specific objectives (both financial and non-financial), defined according to the SMART criteria (Simple, Measurable, Achievable, Relevant, Time-bound),

- scope of implementation, including an assessment (recommended minimum of 3 options; cost-benefit analysis in financial terms; analysis of benefits that cannot be quantified; recommendation of the best option),

- Project financing (optional section) – identification of the source of funding, recommendations for contracts with suppliers (key contract clauses, proposed payment system, contract duration, incentives for those involved),

- the method for achieving the objective (a project plan at an acceptable level of detail), “milestones,” interdependencies with other projects, an outline of a contingency plan (in case of delays, for example), key risks, and proposed methods for mitigating them.

Defining Objectives

The strategic objective of our example project could be, for example, to optimize and standardize the company’s human resources management processes. Specific objectives might include:

A. Optimizing and standardizing HR processes within the company, including:

- optimization of the recruitment process through the use of workflow mechanisms (cost reduction of X),

- Optimization of the leave request approval process (workflow, employee and manager self-service) – shortening the duration of the process and reducing costs by X annually,

- Optimization of the business travel management process (workflow, employee and manager self-service) – shortening the process duration and reducing costs by X annually.

B. Reducing HR operating costs by decreasing the labor intensity:

- processing the regular payroll (on average, 5 to 2 days),

- payroll processing time (on average, from 2 days to 0.5 days),

- preparing documents for ZUS and the Tax Office (from 2 days to 0.5 days),

- managers’ planning of personnel costs through the introduction of an IT tool (reducing the time required from an average of 10 days to 2 days),

- annual salary adjustments by introducing an IT tool (reducing the time required from an average of 5 days to 0.5 days),

- preparing the XYZ report for the corporation (from 2 days to 0.2 days).

C. Reducing the costs of maintaining and developing the system by:

- shifting the burden of adapting the HR system to legislative changes to the vendor (as part of the service fee) (reducing costs from X to Y per year),

- discontinuing the maintenance and development of the following interfaces: HR with the FI/CO system (cost reduction of X per year) and HR with an external time-tracking system (cost reduction of X per year),

- the elimination of some of the company’s systems/platforms (cost reduction of X per year). These are just examples of business objectives that require substantiation (is this possible?) in BC.

The AHP Method

AHP (Analytic Hierarchy Process) is one of the most transparent decision-support methods. AHP is based on the premise that, when making decisions, the experience and knowledge of experts are just as important as the data they use. This method was designed to:

- structuring a multi-criteria decision-making problem,

- prioritizing the various aspects of the problem (criteria and alternatives) in order to rank the alternatives (from best to worst based on the specified criteria).

An unquestionable advantage of the AHP method is that it does not require the direct assignment of weights to individual criteria and alternatives, but operates exclusively on relative evaluations of the elements being compared (all comparisons are made in pairs—based on objective or subjective ratings).

The decision-making process in AHP consists of two phases: hierarchy construction and evaluation. Hierarchy construction requires experience and knowledge of the subject area. Two experts may construct two different hierarchies for the same problem. The best approach here is for a group of experts to work together to reach a consensus on both the design of the hierarchy and the evaluation.

At the top of the hierarchy is the objective of the decision-making process (e.g., selecting an IT solution); at the next levels are the decision criteria and subcriteria; and at the lowest level are the available options (e.g., solutions available on the market).

The evaluation phase involves comparing pairs of elements (criteria, alternatives) at the same level, one by one, from the perspective of the elements defined at the level immediately above. It is advisable to support the AHP decision-making process with one of the available IT solutions (including those offered by BCC—currently All for One Poland).

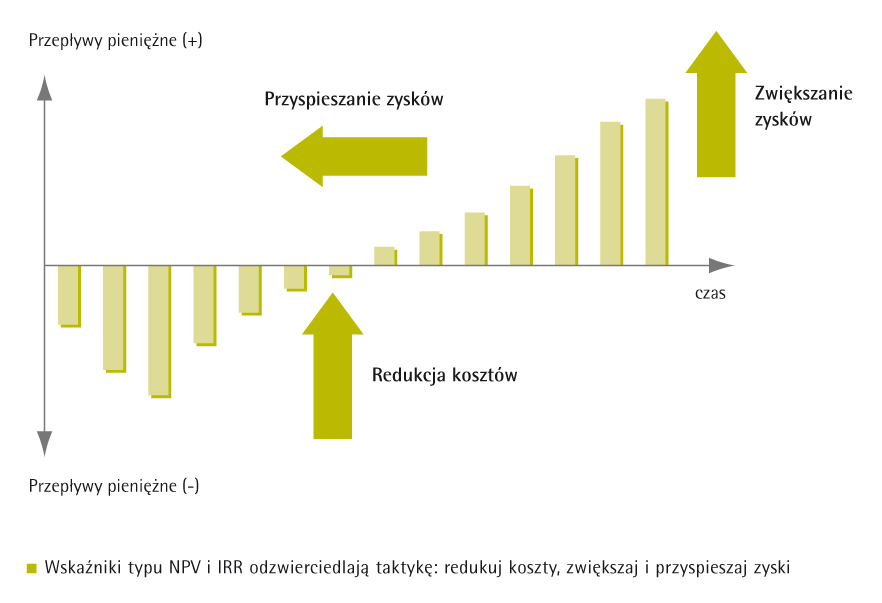

What financial metrics?

BC recipients often expect specific financial indicators that can directly support their decisions. The analysis should show cash flows over a specific period and the method used to calculate benefits and costs. The latter is important because BC always requires certain assumptions and discretionary decisions.

Different teams working independently may obtain different BC results; therefore, to evaluate them, it is necessary to understand the preparation method.

The purpose of the business case is to answer the fundamental question: What will be the financial and business implications of deciding to implement the system?

The most commonly used financial indicators—which also serve as decision-making criteria in business case analyses—are:

- net cash flows,

- net present value (NPV),

- payback period,

- return on investment (ROI),

- discounted cash flow (DCF),

- internal rate of return (IRR),

- total cost of ownership (TCO),

- return on assets (ROA).

Some of the above (e.g., payback period) are static criteria, meaning they do not take into account the time value of money. Their usefulness is limited to evaluating short-term investments.

For large projects (such as the implementation of an SAP system), which are often spread out over time, it is important to take investment opportunities into account. This is made possible by what are known as dynamic criteria. Among these, NPV and IRR are the most commonly used.

The box below provides brief definitions of the most common indicators. For a detailed interpretation, I refer readers to the extensive literature on the subject.

Finally, a few tips

Typically, the ultimate goal of a business analysis is to secure funding for the proposed project. The chances of success will be greater if the authors of the business analysis follow a few simple rules:

- The document should be interesting to the reader—therefore, knowing your audience before beginning the analysis can be helpful,

- It is worth outlining a vision of the project’s outcome so that the reader can see the consequences of the recommended decision,

- Not everything can be quantified in financial terms; the BC should also highlight intangible benefits,

- If the goal of BC is to choose one of several solutions, it is worth supporting the decision-making process with one of the available decision-support methods, such as AHP (Analytic Hierarchy Process).